The 529 Plan Your Broker Sold You May Not Be the Best One

By Todd Stankiewicz | CIO, SYKON Capital | Portfolio Manager, Free Markets ETF (FMKT)

A few weeks ago, I witnessed a conversation between a financial advisor and a prospective client. The client had questions about a 529 college savings plan the advisor was recommending. What struck me was not the questions being asked. It was what the advisor did not seem to know. Nowhere in the conversation was there any mention of state-direct 529 plans. That omission, whether intentional or not, may be costing that family real money.

Two Worlds of 529 Plans

Most people assume a 529 plan is a 529 plan. But there are actually two distinct categories: broker-sold (or advisor-guided) plans and state-direct plans. The difference between them is significant, and every parent saving for college should understand it before opening an account.Broker-sold plans are distributed through financial advisors and brokerage firms. They typically carry commission structures, meaning you pay a sales load every time you contribute. For A-share plans, front-end loads can range from 3.5% to 5.75%. That means for every $1,000 you contribute, you may immediately lose $35 to $57.50 before a single dollar is invested. Annual expense ratios for these plans also tend to be substantially higher than their direct-sold counterparts.

State-direct plans are sold directly to investors without a broker in the middle. You open the account online, typically in under 30 minutes. There are no commissions, no sales loads, and often very low annual expense ratios.

New York: A Case Study in the Cost Difference

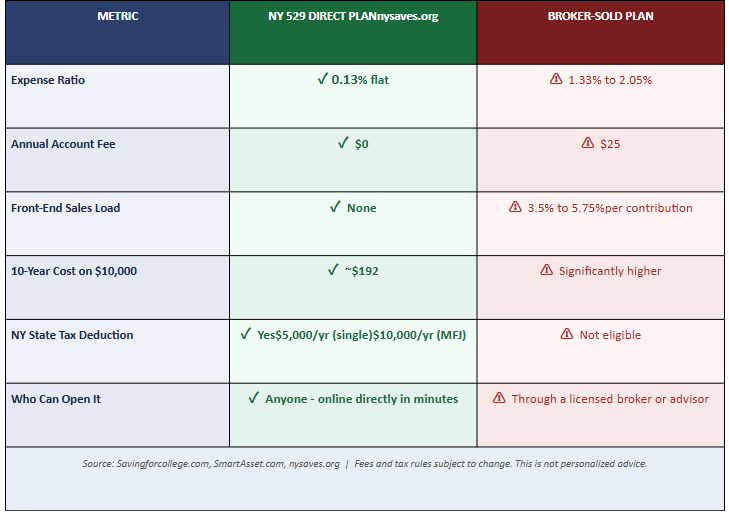

New York illustrates this contrast clearly. The advisor-guided plan carries total annual asset-based fees ranging from approximately 1.33% to 2.05%, plus a $25 annual account maintenance fee. A-share purchases add that upfront commission on every contribution.Then there is the NY 529 Direct Plan, available at nysaves.org. Managed by Vanguard, it carries a flat 0.13% expense ratio and no annual account maintenance fee. According to Savingforcollege.com, the 10-year cost on a $10,000 investment in the direct plan is approximately $192.

Now here is where it gets especially important. New York State offers a tax deduction for contributions to the NY 529 Direct Plan. Single filers can deduct up to $5,000 per year. Married couples filing jointly can deduct up to $10,000. But you only qualify for that deduction if you contribute to New York's own plan. If a New York resident is in a nationally distributed broker-sold plan, they are almost certainly missing that deduction entirely, year after year.

I have seen this scenario play out repeatedly: New York residents in broker-sold plans, paying commissions on every contribution, paying meaningfully higher expense ratios, and leaving the state tax deduction on the table. Many states beyond New York offer similar deductions, available only to residents who invest in their own state's plan.

BY THE NUMBERS

NY 529 Direct Plan vs. Broker-Sold Plan - Key Metrics Side by Side

Why Your Advisor May Not Mention the Direct Plan

Many broker-dealer-affiliated advisors are not permitted to recommend state-direct 529 plans. Those plans do not pay commissions and do not exist on the firm's approved product list. Recommending one outside of that list could be considered "selling away," a compliance violation in the traditional broker-dealer world. The advisor may not be aware of the direct option, or may be restricted from recommending it even if they are.This is not a criticism of every advisor in that model. But if you are working with a commission-based advisor, it is worth asking directly: are there direct-sold alternatives I should be considering?

529s Have Built-In Limitations That Make Fees Matter Even More

Per IRS rules, you can only reallocate your existing 529 investments twice per calendar year. Tactical management is not really an option. For most families, an age-based portfolio, one that automatically shifts from growth to more conservative allocations as the child approaches college age, is the most practical approach.When the investment strategy is largely on autopilot, the variables that most impact long-term outcomes are how much you contribute, how consistently you contribute, and how much you pay in fees. That is why the cost difference between a direct plan and a broker-sold plan can compound so meaningfully over 15 to 18 years.

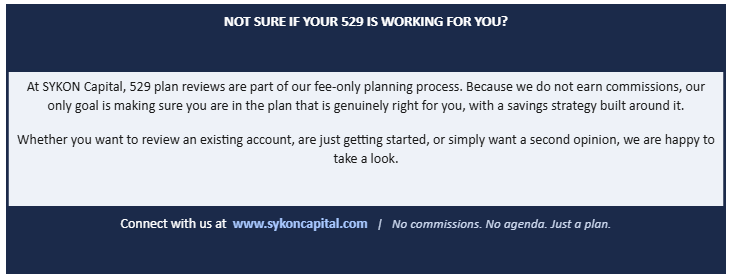

The SYKON Capital Approach

At SYKON Capital, we are fee-only and do not earn commissions on any investment product. That independence matters, especially with 529 planning. When a client comes to us, one of the first things we look at is whether they are in the right plan for their state. In the vast majority of cases, particularly for New York residents, we guide families toward the state direct-sold plan. The math is simply too compelling to recommend otherwise.Where we earn our keep is in the planning itself: helping you figure out how much to save, how to build a contribution schedule that fits your life, and how to think about 529 funding as part of your broader financial plan. If you have an existing 529 and are not sure whether it is the right plan for you, or if you have never opened one and do not know where to start, that is exactly the kind of conversation we are here to have. There is no commission on the line. Just honest guidance.

Two Powerful Strategies Worth Knowing

Here is a lesser-known approach worth considering, especially for those who do not yet have children but know they want to in the future. You can open a 529 plan and name yourself as both the account owner and the beneficiary. Once a child is born, you can change the beneficiary to that child. The advantage is straightforward: you get a longer runway for compounding. Rather than starting the clock at birth with under 18 years to save, you could add several years to your timeline, meaning each dollar has more time to grow and you may need to save less overall.But here is where it gets even more interesting. Starting early may also give you additional flexibility under relatively new federal legislation.

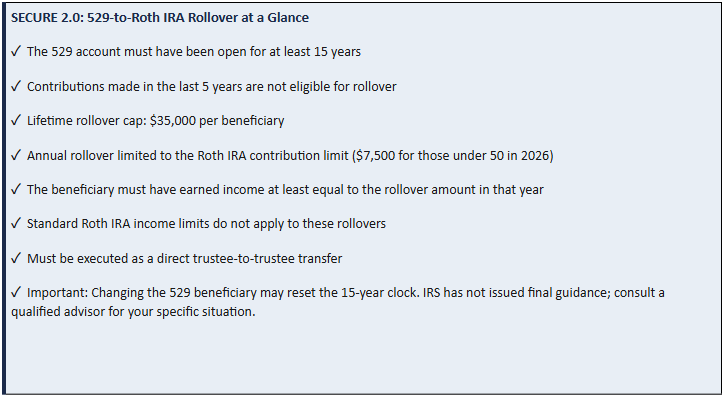

Under the SECURE 2.0 Act, effective January 1, 2024, unused 529 plan funds may be eligible to be rolled over into a Roth IRA for the account beneficiary, tax-free and penalty-free. This is a meaningful development for families who overfund a 529 or whose child receives a scholarship, takes a different educational path, or simply does not use all of the funds saved.

This is one more reason why starting a 529 early, even before a child is born, matters. The 15-year clock begins from the date the account is established. The earlier you start, the sooner you may reach eligibility for this rollover option, and the more flexibility you preserve. If you later change the beneficiary to your child, note that the 15-year timeline may reset from the date of that change. This is an area where coordinating with a qualified financial and tax advisor is particularly important.

The Bottom Line

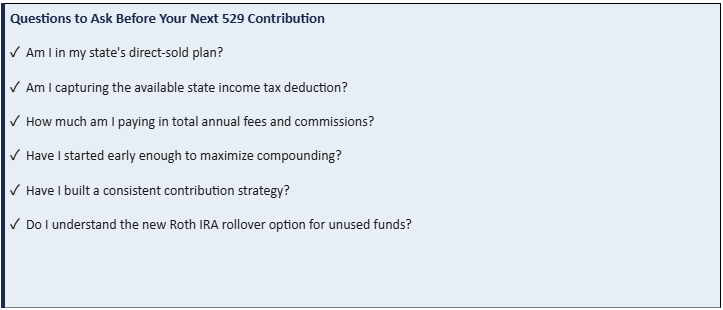

529 plans are one of the most powerful tools available for funding education. But not all plans are created equal. Before opening one, or continuing to contribute to one you are already in, consider asking yourself:

The answers to those questions could be worth tens of thousands of dollars over the course of your savings timeline.

Email me at todd@sykoncap.com with any questions about your plan

About the Author

Todd Stankiewicz is Chief Investment Officer of SYKON Capital, a fee-only registered investment advisory firm with offices in Westchester County, NY and Jupiter, FL. As a fee-only advisor who earns no commissions on any investment product, Todd works with families to evaluate whether their existing savings and investment vehicles are structured in their best interest, including college savings strategies, 529 plan selection, and education funding as part of a broader financial plan. He has helped New York-area and Westchester County families identify potentially costly mismatches between their current 529 plans and the direct-sold alternatives available to them.

SYKON Capital is a fee-based RIA registered with the U.S. Securities and Exchange Commission. Learn more at www.sykoncapital.com or reach Todd directly at todd@sykoncap.com.

April 23, 2026

Questions People Are Searching About This Article

Q: What is the difference between a broker-sold 529 plan and a direct-sold 529 plan?

Broker-sold 529 plans are distributed through financial advisors and brokerage firms. They typically carry front-end sales loads (commissions) plus higher ongoing expense ratios when comapred to direct sold plans. Direct-sold plans are purchased directly from the state, with no broker in the middle, typically no sales commissions, and usually significantly lower fees. For most families, especially those in states with strong direct-sold options, the direct plan is worth a serious look before opening or continuing to fund a broker-sold account.

Q: Do New York residents get a tax deduction for 529 contributions?

Yes, but only if you contribute to New York's own state-sponsored plan. New York offers a state income tax deduction of up to $5,000 per year for single filers and up to $10,000 for married couples filing jointly, but the deduction applies exclusively to contributions made to a NY 529 Plan. New York residents who are invested in a nationally distributed broker-sold plan typically will not be eligible for this deduction, regardless of how long they have been contributing. That means they may be paying higher fees and potentially losing a meaningful annual tax benefit simultaneously. Many other states offer similar deductions tied to their own in-state plans. Before assuming your current plan qualifies, verify with a financial or tax advisor whether your state of residence offers a deduction and whether your current plan is eligible for it.

Q: What happens to leftover money in a 529 plan if my child does not use it?

Under the SECURE 2.0 Act, effective January 1, 2024, unused 529 funds may be eligible for a tax-free, penalty-free rollover into a Roth IRA for the account beneficiary. To qualify, the 529 account must have been open for at least 15 years, and annual rollovers are subject to Roth IRA contribution limits. This is a meaningful development for families who overfund a 529, whose child receives a scholarship, or whose child takes a different educational path. It transforms the 529 from a use-it-or-lose-it vehicle into a potentially more flexible long-term savings tool. One important note: the 15-year clock starts from when the account was originally established, not from when the child was born. Starting a 529 early, even before a child arrives, can help preserve maximum flexibility down the road.

This content is for informational and educational purposes only and should not be construed as personalized financial, tax, or investment advice. Tax laws, plan details, and IRS guidance are subject to change. Fee figures referenced are based on publicly available sources and may vary. Please consult a qualified financial or tax professional before making any investment or tax decisions. SYKON Capital is a registered investment adviser.

For informational and educational purposes only. SYKON Capital is a registered investment adviser.