The Day Private Credit Has to Tell the Truth

By Todd Stankiewicz | CIO, SYKON Capital | Portfolio Manager, Free Markets ETF (FMKT)

Private credit has grown into a roughly $3 trillion industry¹, pitched to retail and high-net-worth investors as a safe, income-generating alternative to public markets. Steady yields, low volatility, minimal correlation to stocks. The sales pitch worked. Money poured in.

Now the redemption wave is here, and in our view, it is accelerating in a way that deserves close attention.

The Numbers Are Hard to Ignore

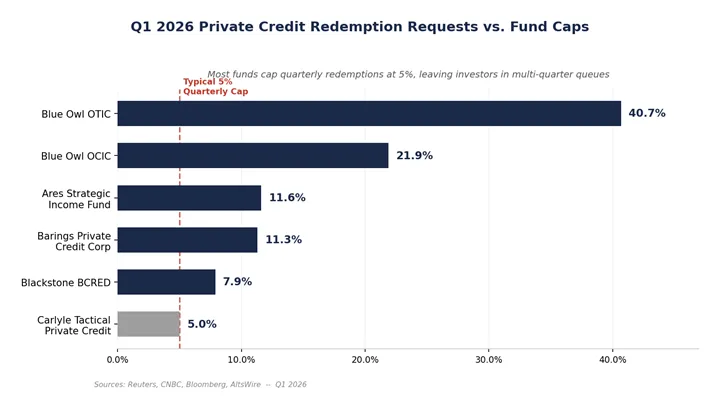

In Q1 2026 alone, over $13 billion in redemption requests hit major private credit funds². Here is what happened at some of the largest names in the space:Blue Owl Capital saw investors request to pull 40.7% of shares from OTIC (Blue Owl Technology Income Corp) ³ and 21.9% from OCIC (Blue Owl Credit Income Corp) ⁴, totaling roughly $5.4 billion in redemption requests⁵. The funds capped quarterly redemptions at 5%, leaving approximately $4.6 billion trapped⁶. To meet even those capped redemptions, Blue Owl sold about $1.4 billion in loan assets at 99.7 cents on the dollar to institutional buyers including CalPERS, OMERS, and BCI⁷. OBDC II (Blue Owl Capital Corp II) halted quarterly redemptions entirely and moved to a mandatory wind-down structure⁸. Blue Owl’s stock hit all-time lows⁹.

Figure 1: Q1 2026 redemption requests across major private credit funds, compared to the standard 5% quarterly cap.

Blackstone’s flagship $82 billion BCRED fund faced a record 7.9% in redemption requests, roughly $3.8 billion gross¹⁰. Blackstone raised its redemption cap from 5% to 7% and injected $400 million of firm capital to meet all requests¹¹. Net outflows came in at approximately $1.7 billion after accounting for $2 billion in new inflows¹².

Ares gated its approximately $22 billion Strategic Income Fund after redemption requests reached 11.6% in a single quarter¹³. Carlyle capped redemptions at 5% of its Carlyle Tactical Private Credit Fund¹⁴.

Adding to the pressure, JPMorgan marked down loans to certain private credit funds¹⁵, and activist investor Boaz Weinstein’s Saba Capital launched a tender offer for Blue Owl BDC shares at 20% to 35% below reported NAV¹⁶. We think that bid speaks volumes about where actual market clearing prices may sit relative to stated valuations.

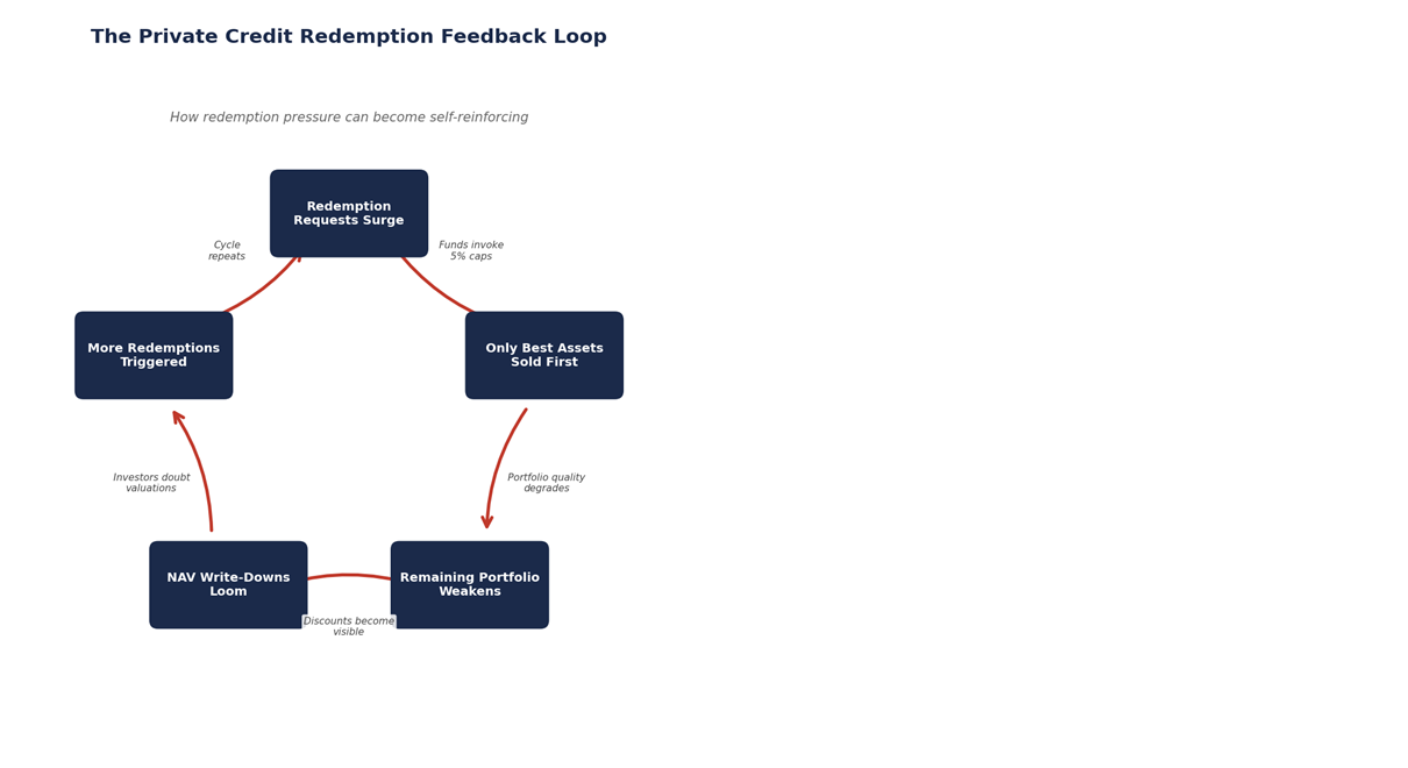

The Negative Feedback Loop We Believe Is Building

Here is the mechanism we are watching closely, and why we think the risk is not yet fully appreciated.First, redemption requests surge. This is happening now, across multiple large funds simultaneously. Second, funds invoke quarterly caps, typically around 5%, meaning the vast majority of investors who want out cannot get out. Third, to meet even those capped redemptions, fund managers have limited options: draw on credit lines, use incoming cash from new investors, or sell loans.

This is where it could get problematic. When managers sell, they naturally sell the most liquid, highest quality loans first. These are the ones that trade near par. Blue Owl’s initial sales at 99.7 cents on the dollar illustrate this perfectly. The best paper goes out the door.

But quarter after quarter, as redemptions persist, the remaining portfolio may skew increasingly toward less liquid, smaller, and potentially lower quality positions. These are the loans nobody wanted to buy in the first round.

Eventually, if pressure continues to mount, remaining loans may need to be sold at meaningful discounts. Buyers know this. Saba Capital’s offer at 20% to 35% below NAV is, in our view, a preview of what happens when sophisticated buyers sense a forced seller across the table. They put in lowball bids and wait.

If private credit loans begin trading at real discounts, it could force mark-to-market questions across the entire sector. Funds holding similar loans may need to write down their stated NAVs. And that potential contagion effect could trigger another wave of redemptions from investors who suddenly doubt the valuations in their own funds.

That is the loop. Redemptions lead to asset sales. Asset sales degrade portfolio quality. Degraded quality and visible discounts could trigger more redemptions. And the cycle may continue.

Figure 2: The self-reinforcing redemption cycle in private credit funds under sustained outflow pressure.

What Concerns Us Most: The Risk for Remaining Investors

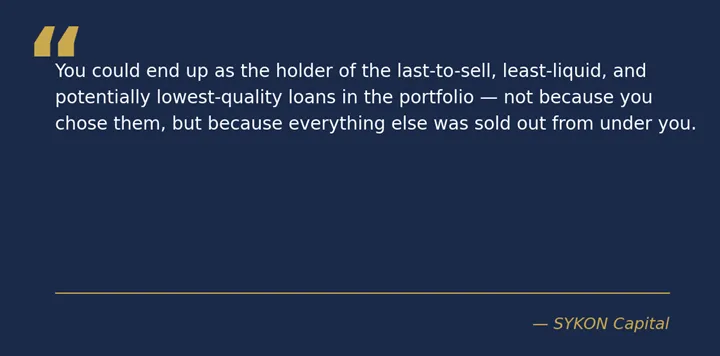

If you hold a position in one of these funds and are not redeeming, we believe you should understand what may be happening to the composition of your holdings.Fund managers are rational actors. They sell what they can sell easily first. That means the highest quality, most liquid loans are likely being sold to meet departing investors’ redemptions. What may stay behind? The smaller positions, the less liquid credits, the loans where there may not be a ready buyer at par.

Even if you believe in private credit as an asset class, the mechanics of these redemption queues could create a hidden risk: the composition of what you actually own may be quietly degrading with every passing quarter. You could end up as the holder of the last-to-sell, least-liquid, and potentially lowest-quality loans in the portfolio, not because you chose them, but because everything else was sold out from under you.

About the Author

Todd Stankiewicz is Chief Investment Officer of SYKON Capital, a registered investment advisory firm with offices in Westchester County, NY and Jupiter, FL. As CIO, Todd leads portfolio construction, risk management, and investment strategy for the firm's client base, with direct experience helping investors navigate gated alternative structures including BREIT and Starwood. His work focuses on helping to identify structural risks in investment products before they become client problems, including liquidity mechanics, redemption dynamics, and valuation integrity in private markets. Todd also serves as Portfolio Manager of the Free Markets ETF (FMKT), a publicly traded fund focused on deregulation-driven investment themes.

SYKON Capital is a fee-based RIA registered with the U.S. Securities and Exchange Commission.

April 21, 2026

What Should Investors Be Asking?

At SYKON Capital, we have worked with investors navigating exactly this kind of situation before, when gating mechanisms in prior private fund structures left clients uncertain about timelines, valuations, and next steps. The following questions are the ones we believe every investor in a gated or near-gated fund should be asking their manager directly.

We are not arguing that private credit is broken. But we believe the redemption mechanics playing out right now create specific, identifiable risks that investors and advisors should be pressure-testing directly with their fund managers. Here are the questions we think matter most.

1. What percentage of the original portfolio has been sold over the last two to three quarters to meet redemptions, and what types of loans were sold first?

Why it matters: Funds sell the most liquid, highest-quality loans first because those are the ones they can move near par. What leaves the portfolio tells you more about what stays than any fund fact sheet will. If the best paper is already out the door, remaining investors may be holding a fundamentally different book than the one they bought into.

2. How many quarters deep is the redemption queue right now, and what is the estimated wait time for a full redemption at the current pace?

Why it matters: A 5% quarterly cap on a fund with 20% to 30% of assets in redemption requests could mean a four-to-six-quarter wait, or longer. That is not quarterly liquidity. That is a multi-year exit process, and investors should understand the difference before assuming they can get out when they need to.

3. Is the fund using credit lines or subscription facilities to fund redemptions, and if so, how much capacity remains?

Why it matters: Tapping credit lines buys time, but it adds leverage to the fund and is not a permanent solution. When that borrowing capacity runs out, the only remaining option is to sell assets. Investors should know how close the fund may be to that threshold.

4. What is the current ratio of new inflows to redemption requests? Is the fund in net inflow or net outflow?

Why it matters: New inflows can help meet redemptions without selling assets. A fund in persistent net outflow has no such buffer and will likely need to sell. The direction of flow matters as much as the level of redemptions.

5. How has the average loan size, credit rating, or sector concentration of the portfolio changed over the last two to three quarters?

Why it matters: If the composition is quietly drifting toward smaller, less liquid, or more concentrated positions, it could be a signal that the best paper has already been sold out. Portfolio drift may not show up in headline metrics, but it changes the risk profile of what remains.

6. What percentage of loans in the portfolio are PIK (payment-in-kind), meaning interest is being added to principal rather than paid in cash?

Why it matters: PIK loans can mask stress. A borrower paying in-kind may not have the cash flow to service the debt at all. Rising PIK concentration could be an early warning sign of portfolio quality deterioration, and it is worth tracking quarter over quarter.

7. Has the fund’s NAV been independently verified or stress-tested against where comparable loans are actually trading in the secondary market?

Why it matters: Saba Capital’s offer to buy Blue Owl BDC shares at 20% to 35% below stated NAV is a data point worth taking seriously. If sophisticated buyers believe stated valuations are too high, remaining investors may be carrying more risk than the NAV suggests. We think it is reasonable to ask how the fund’s marks compare to where similar loans are actually clearing.

8. What is my actual all-in return if I account for reduced liquidity, the time value of money in a redemption queue, and the potential for declining NAV as less liquid assets remain?

Why it matters: A 9% to 10% stated yield means less when capital is locked up for an uncertain period and the assets backing it may need to be sold at a discount. We believe investors should be calculating their risk-adjusted return with the full picture in view, not just the headline number.

We think these questions are reasonable, and we think the answers matter. Private credit may still have a role in portfolios, but in our view, investors who are not actively pressure-testing their fund managers on liquidity, composition, and valuation risk could be the ones most exposed when the next chapter of this story plays out. The cost of not asking may be higher than the cost of an uncomfortable conversation.

Is Your Portfolio Caught in a Gate?

If you hold a position in a private credit fund that is gating, queuing, or restricting your access to capital, now is the time to act with clarity rather than wait in uncertainty.At SYKON Capital, we have helped investors evaluate holdings and develop exit strategies when fund gates have closed in the past. We understand the mechanics of redemption queues, secondary market discounts, and portfolio composition drift because we have navigated these situations with clients before. You do not need to figure this out alone.

If you have questions about what your private credit holdings actually look like today, what your realistic exit options are, or simply want a second opinion on how your fund is managing this environment, we welcome that conversation.

Here is how to reach us:

Visit our website: www.sykoncapital.com

Schedule a complimentary consultation

Email us directly: todd@sykoncap.com

The questions you ask today could be the difference between protecting your capital and being the last one out the door. Reach out to us. We are here to help.

Sources

¹ Congressional Research Service, “Private Credit Funds Redemption Restrictions: Market Context and Policy Issues,” April 2, 2026 (CRS IN12674)² Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026; WealthManagement.com

³ Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026

⁴ Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026

⁵ Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026

⁶ PipelineRoad, “Blue Owl Caps Redemptions on Two BDCs After Q1 Surge,” April 2, 2026

⁷ Bloomberg, “Blue Owl Fund Urges Shareholders to Reject Tender from Saba, Cox,” March 13, 2026

⁸ Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026

⁹ Reuters, “Blue Owl limits withdrawals from two funds after historic surge in redemption requests,” April 2, 2026

¹⁰ CNBC, “Blackstone’s Gray: Market ‘noise’ fueled record redemptions from world’s largest private credit fund,” March 3, 2026; Morningstar, “Blackstone Private Credit Aims to Calm Investor Jitters,” 2026

¹¹ Morningstar, “Blackstone Private Credit Aims to Calm Investor Jitters,” March 3, 2026

¹² Private Equity Wire, “Blackstone credit fund meets record 7.9% redemption requests,” 2026; Morningstar, “Blackstone Private Credit Aims to Calm Investor Jitters,” 2026

¹³ Reuters, “Ares caps withdrawals at private credit fund after redemption requests surge,” March 24, 2026

¹⁴ Congressional Research Service, “Private Credit Funds Redemption Restrictions: Market Context and Policy Issues,” April 2, 2026 (CRS IN12674)

¹⁵ Reuters, “Private credit jitters trigger caps on redemptions, tighter lending,” April 2, 2026

¹⁶ Bloomberg, “Saba and Cox Announce Tender Offers for Blue Owl BDC Shares,” February 20, 2026

Advisory Services offered through SYKON Capital LLC, a registered investment advisor with the U.S. Securities and Exchange Commission. This material is intended for informational purposes only. It should not be construed as legal or tax advice and is not intended to replace the advice of a qualified attorney or tax advisor. The information contained in this presentation has been compiled from third party sources and is believed to be reliable as of the date of this report. Past performance is not indicative of future returns and diversification neither assures a profit nor guarantees against loss in a declining market. Investments involve risk and are not guaranteed.