The S&P 500 May Be Changing. Do Investors Know What They Own?

By Todd Stankiewicz | CIO, SYKON Capital | Portfolio Manager, Free Markets ETF (FMKT)

Most investors use the S&P 500 as shorthand for “the market.” That makes sense. It is widely followed, easy to access, and has become the foundation for many long-term investment portfolios.

But the S&P 500 is not a fixed object. It is an index with rules, eligibility standards, committee decisions, and periodic methodology changes. When those rules evolve, the exposure investors receive can evolve with them.

That is why a current proposal from S&P Dow Jones Indices deserves attention.

S&P Dow Jones Indices is reviewing potential changes to how megacap companies may qualify for major U.S. benchmarks, including the S&P 500. The discussion appears tied to a broader shift in public markets: some of the largest and most influential companies may come public much later in their life cycle, at much larger valuations, and in some cases before they meet the profitability profile investors have historically associated with S&P 500 inclusion.

The proposal has not been finalized. That distinction matters. But even as a proposal, it raises an important question for investors: if the index changes, do you still understand what you own?

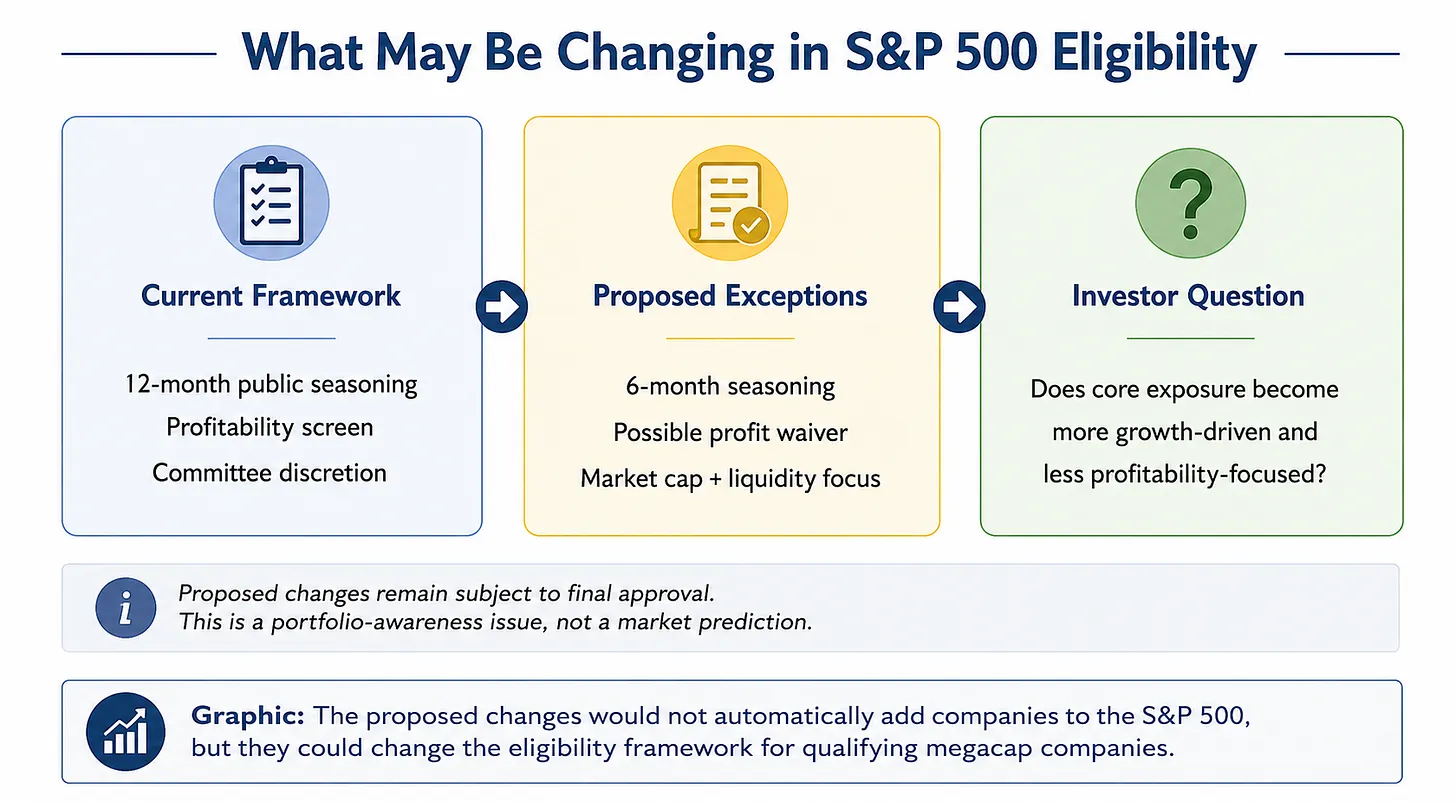

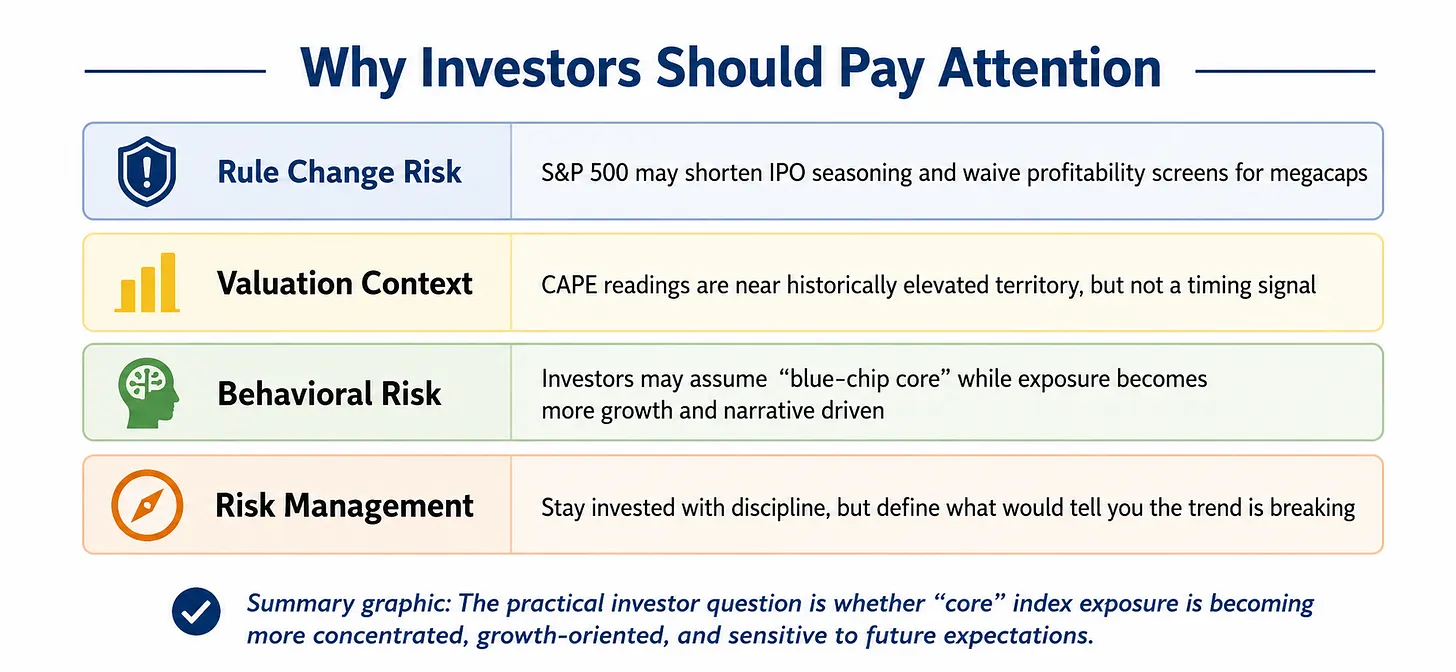

The key changes under discussion are fairly direct. Reporting indicates that S&P DJI is considering reducing the seasoning period for newly public companies from 12 months to six months before they may become eligible for index inclusion. S&P DJI is also considering whether large-cap or megacap companies should be exempt from certain profitability requirements.

In plain English, that could mean some very large newly public companies may qualify for index consideration sooner, even if they have not yet demonstrated the same profitability record that investors typically associate with “blue-chip” status.

This is not automatically a bad thing. Markets change. Companies are staying private longer. By the time firms such as SpaceX, OpenAI, or Anthropic eventually pursue public listings, they may already be among the most economically relevant companies in the world. If an index is supposed to reflect the investable market, there is a reasonable argument that it should adapt to that reality.

Nasdaq has already moved in a similar direction. Its Nasdaq-100 methodology updates took effect on May 1, 2026, and include a fast-entry framework that can allow qualifying newly listed companies to enter after the 15th trading day. That is a meaningful change from a slower, more seasoned approach to index inclusion.

So the issue is not whether index rules should evolve. The issue is whether investors understand the trade-offs.

The S&P 500 has never been a pure quality index. It is market-cap weighted, committee-governed, and naturally influenced by the largest companies in the market. Still, profitability standards have historically helped reinforce the perception that the index represents established, seasoned businesses.

If those standards are loosened for megacap companies, the S&P 500 may become more responsive to the largest growth stories in the market. That may improve representation, but it may also make the index more exposed to companies whose valuations depend heavily on future expectations rather than current earnings.

That distinction matters because many investors do not think about index construction. They simply own an S&P 500 ETF, a Nasdaq-100 fund, a large-cap growth fund, and maybe a technology or AI-themed strategy and assume they are diversified. In reality, those exposures may overlap more than they realize.

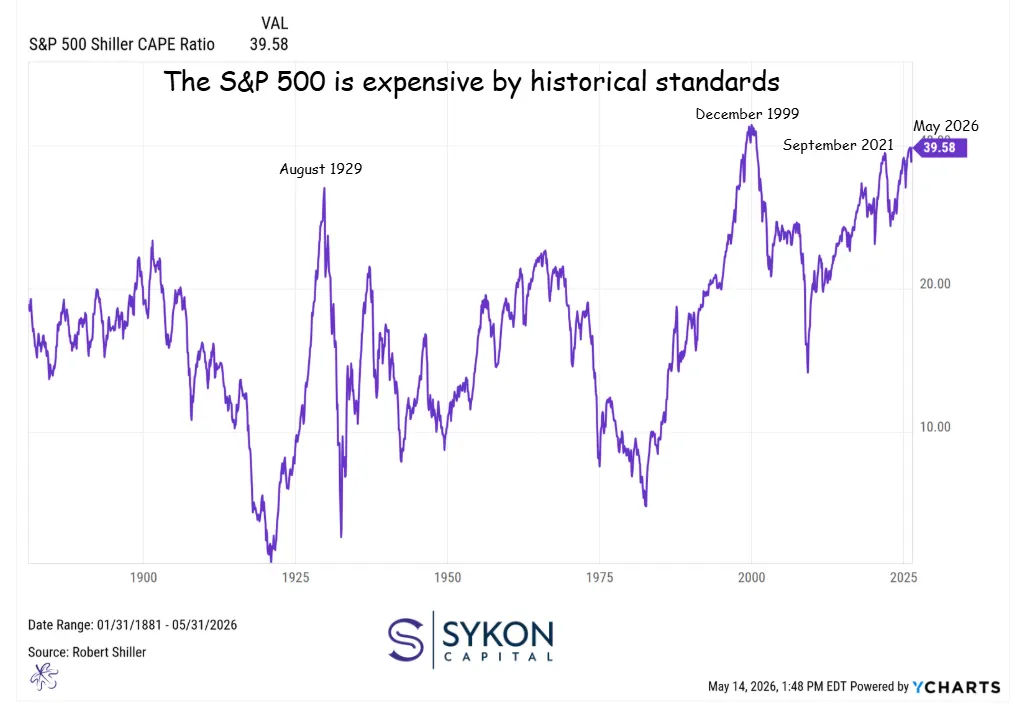

This becomes even more relevant when valuations are already elevated. The Shiller CAPE ratio, which compares the S&P 500’s price to a 10-year average of inflation-adjusted earnings, has recently been near historically high levels. Different providers calculate the current figure slightly differently, but recent readings have clustered around the high 30s to roughly 40. For context, CAPE readings were also elevated near the late-1990s and 2000 dot-com peak.

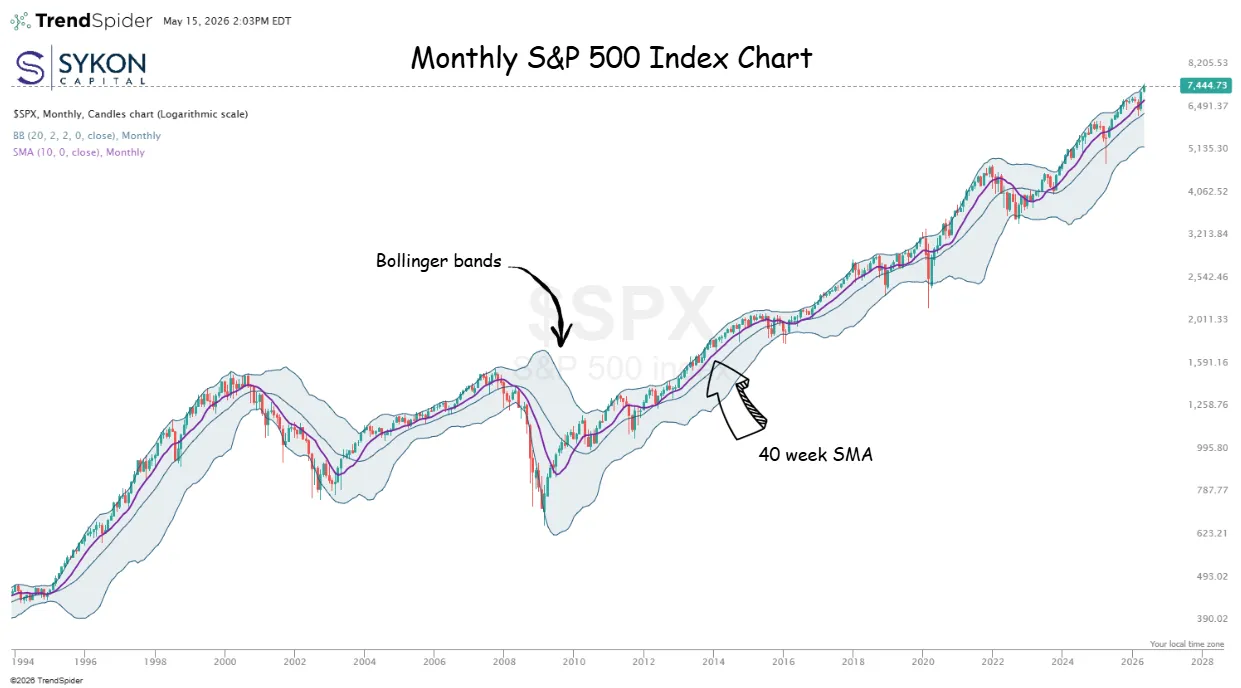

To be clear, CAPE is not a timing tool. A high valuation does not tell you a market has to fall tomorrow, next month, or even this year. Strong markets can remain strong for longer than skeptical investors expect. The current long-term trend in the S&P 500 remains constructive, especially when viewed through a monthly technical lens.

That is exactly why risk management matters.

The goal is not to spend every week trying to call the top. That is not a disciplined process. The goal is to participate when the trend is healthy while having a framework that helps identify when the market’s character is changing.

Technical analysis can be useful here. A monthly S&P 500 chart can help investors focus on bigger-picture signals instead of daily noise. Are prices holding key trend levels? Is market breadth confirming the index? Are leadership stocks still leading? Are momentum indicators weakening while prices push higher? These questions become more important when valuations are elevated and index construction may be shifting toward more growth-sensitive exposure.

The real risk is not that one famous company eventually enters the S&P 500. The bigger risk is that investors assume their portfolio is more balanced than it actually is.

If the S&P 500 becomes more open to newly public megacaps, and if those companies are tied to the same artificial intelligence, technology, and future-growth themes already dominating large-cap benchmarks, investors may be taking more concentrated exposure than they realize.

This is not a reason to abandon indexing. It is a reason to understand indexing.

At SYKON, this is the kind of issue we pay close attention to because it sits at the intersection of portfolio management, index construction, ETF strategy, and market behavior. We are not simply asking whether an investor owns “the market.” We are asking what that market exposure actually represents, how concentrated it has become, and what signals would suggest the risk profile is changing.

That perspective matters. Many investors receive passive allocation advice, but fewer receive a true portfolio-construction review that considers overlap, index methodology, technical trend structure, valuation context, and risk-management discipline together.

If you are heavily allocated to S&P 500 funds, Nasdaq-100 exposure, large-cap growth, or AI-themed strategies, this may be a good time to review what you actually own. If you want help breaking that down, we can look at it with you. If not with us, get an informed opinion from someone who understands portfolio construction, not just asset allocation labels.

The point is not to overreact. The point is to pay attention.

The S&P 500 may still be the core benchmark for many investors. But if the rules defining that benchmark are changing, investors should understand how those changes may affect their portfolios before the next market cycle teaches the lesson for them.

About the Author

Todd Stankiewicz is Chief Investment Officer of SYKON Capital, a registered investment advisory firm with offices in Westchester County, NY and Jupiter, FL. As CIO, Todd leads the firm's investment strategy with a focus on technical analysis, index construction, portfolio overlap, and risk management discipline. He regularly appears on Fox Business and Schwab Network discussing market structure, ETF strategy, and portfolio positioning. His work centers on helping investors understand not just what they own, but how it behaves in different market environments, including the concentration risks that index-heavy portfolios can quietly accumulate over time. Todd also serves as Portfolio Manager of the Free Markets ETF (FMKT), a publicly traded fund focused on deregulation-driven investment themes.

SYKON Capital is a fee-based RIA registered with the U.S. Securities and Exchange Commission.

FAQ

What S&P 500 rule changes are being discussed?

S&P Dow Jones Indices is reviewing whether megacap companies should be eligible for faster index consideration, including a possible reduction in the IPO seasoning period from 12 months to six months and possible exceptions to profitability requirements.

Are the S&P 500 changes final?

No. Based on current reporting, the changes are proposed and subject to the consultation and approval process.

Why does this matter for investors?

Investors often view S&P 500 exposure as broad, diversified, and blue-chip. If index rules allow faster entry for less-seasoned or unprofitable megacap companies, the character of that exposure may shift over time.

Does this mean investors should sell the S&P 500?

No. This is not a market-timing call or a crash prediction. It is a reminder to understand portfolio overlap, concentration, valuation risk, and the technical signals that would indicate a change in market trend

S&P 500 rule changes, S&P 500 profitability requirement, S&P 500 IPO seasoning period, S&P 500 megacap IPO inclusion, SpaceX IPO S&P 500, OpenAI IPO S&P 500, Anthropic IPO S&P 500, Nasdaq-100 fast entry rule, Shiller CAPE ratio 2026, index investing risk, portfolio overlap, technical risk management, ETF portfolio construction.

Sources and Verification Notes

- S&P Dow Jones Indices consultation timing and proposed implementation date, Reuters-linked summary: https://longbridge.com/en/news/284845425

- Reuters via MarketScreener: S&P DJI considering six-month seasoning and excluding profitability requirements for large-cap companies: https://uk.marketscreener.com/news/s-p-dow-jones-indices-considers-new-index-rules-as-mega-ipos-loom-ce7f58d8d18bf52d

- Bloomberg Law: S&P weighs shorter public-seasoning period and possible profitability/liquidity waivers: https://news.bloomberglaw.com/securities-law/s-p-weighs-new-index-rules-to-speed-up-addition-of-mega-ipos-1

- Reuters: Nasdaq fast-entry rule, 15th trading day, and May 1 effective date: https://www.reuters.com/business/new-nasdaq-rules-include-fast-entry-new-listings-benchmark-index-2026-03-30/

- Nasdaq: Nasdaq-100 methodology update rationale: https://www.nasdaq.com/newsroom/nasdaq100-index-methodology-update-why-now

- Multple: Shiller PE historical table and current readings: https://www.multpl.com/shiller-pe

- GuruFocus: Shiller PE current valuation context: https://www.gurufocus.com/shiller-PE.php

- Todd Stankiewicz