You Made an IRA Contribution You Shouldn't Have. Now What?

By Todd Stankiewicz | CIO, SYKON Capital | Portfolio Manager, Free Markets ETF (FMKT)

A Real-World IRA Mess

A recent post in a popular online personal finance community told a story I've seen play out dozens of times. The poster had made Traditional IRA contributions they shouldn't have, discovered the problem too late, and was now trying to unwind it with recharacterizations, reverse rollovers, and a backdoor Roth conversion. The thread quickly filled with conflicting advice and a growing sense of dread.

This situation is far more common than most people realize. It typically happens to smart, high-earning DIY investors who contribute early in the year and only discover at tax time that their income crept past the limit. By then, the fix is complicated, paperwork-heavy, and sometimes costly.

The good news? Most of this is preventable. As the old saying goes, an ounce of prevention is worth a pound of fixing. Let's walk through how this happens, how to avoid it, and what to do if you're already in the weeds.

How Does This Happen?

The scenario usually goes like this: you contribute to your IRA in January, confident your income falls within the limits. Then life happens. You change jobs, receive a bigger bonus than expected, vest in equity compensation, or your spouse returns to work. When you file taxes in April, you discover your Modified Adjusted Gross Income (MAGI) pushed past the contribution or deductibility threshold.

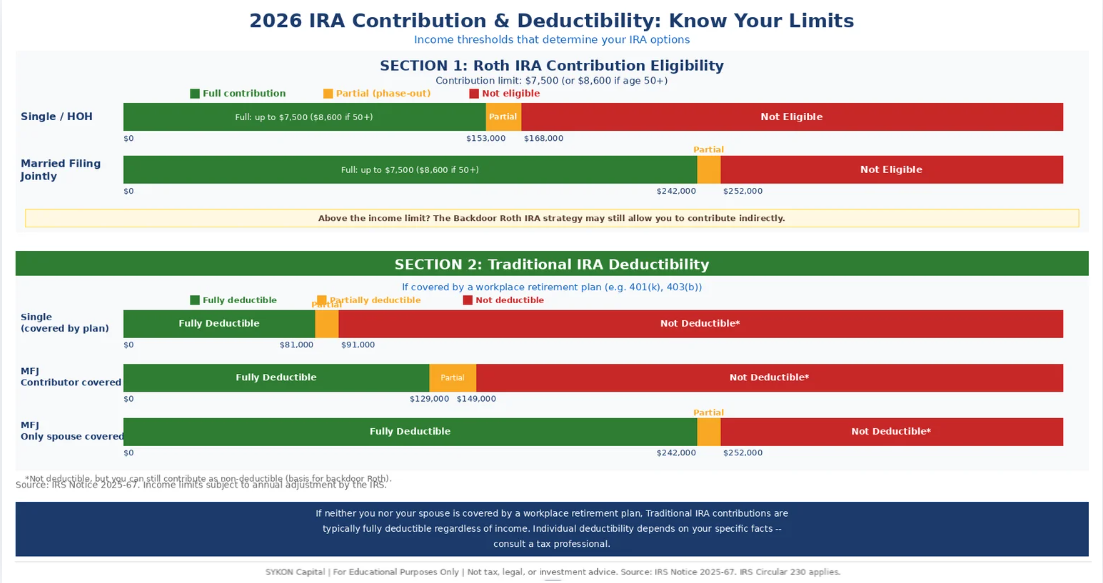

Now you have an excess contribution sitting in an IRA, and the IRS is not going to shrug it off. Here are the 2026 income limits to keep in mind:

Figure 1: 2026 IRA Income Limits at a Glance (Source: IRS Notice 2025-67)

The Smart Move: Wait to Contribute

Here is the simplest, most underrated piece of tax planning advice I can offer: you have until April 15 of the following year to make IRA contributions for the prior tax year. If your income is anywhere near the phase-out ranges, wait. File your taxes first, know your actual MAGI, and then contribute. This one habit can help you avoid the most common IRA contribution mistake. It costs you nothing except a few months of patience.

For people with stable W-2 income well below the limits, contributing early is usually fine. But if you have variable compensation, equity vesting, or a spouse whose income might change, the risk of contributing early is not worth it.

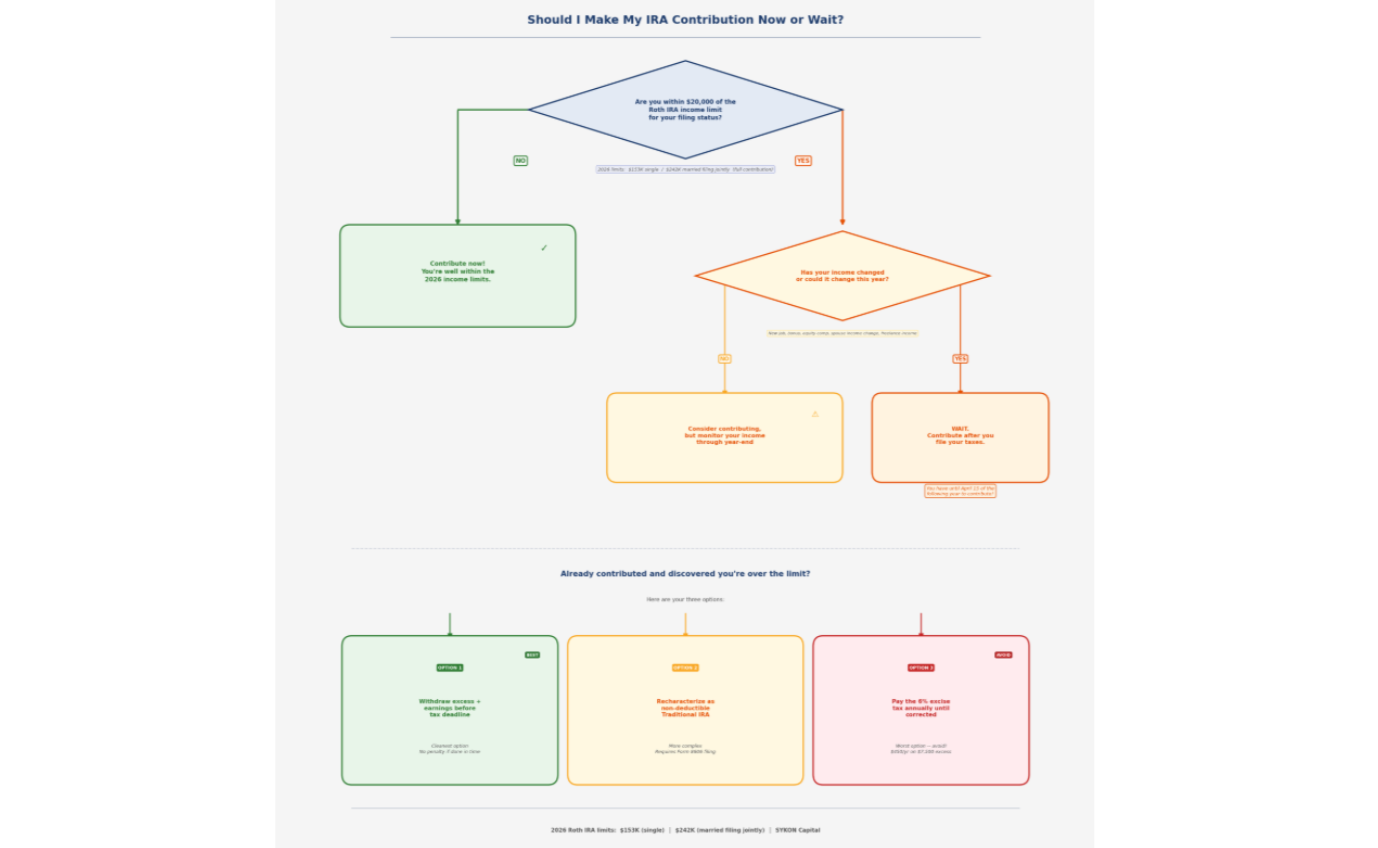

Should I Contribute Now or Wait?

Figure: IRA Contribution Decision Guide (2026)

If It's Already Happened: Your Options

If you've already contributed and your income ended up over the limit, don't panic. You have several paths forward, but you need to act before the tax filing deadline (including extensions in some cases).Recharacterize the contribution. This moves the contribution (and associated earnings) from a Roth to a Traditional IRA, treating it as if the Traditional contribution was made originally. It becomes non-deductible, and you will need to file Form 8606 to document the basis. This is typically the cleanest option if you want to keep the money in an IRA.

Withdraw the excess contribution plus earnings. If done before the tax deadline, you may avoid the 6% penalty. The earnings portion is taxable and may be subject to the 10% early withdrawal penalty if you are under 59 1/2. This may be the right approach if you want a clean slate.

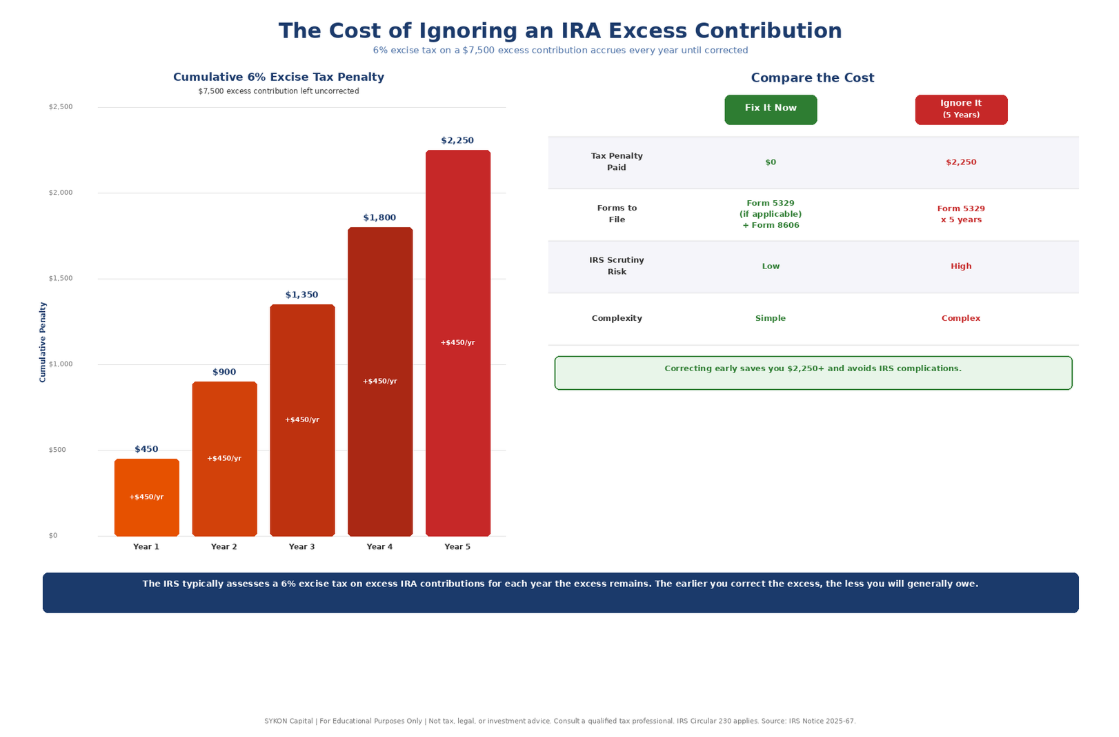

Do nothing and pay the 6% excise tax. This is the worst option. On a $7,500 excess contribution, that is $450 per year, every year you delay.

Figure 2: The Cost of Ignoring an Excess IRA Contribution

Whatever path you choose, get it documented properly. These steps can get complicated, and sloppy recordkeeping is what turns a simple fix into a multi-year headache. Form 8606 should be filed to document non-deductible contributions. If an excess contribution exists and the 6% excise tax applies, Form 5329 is also required.

The Separate Account Trick Nobody Talks About

If you end up with post-tax (non-deductible) contributions in a Traditional IRA, here is a practical tip most people overlook: keep them in a separate IRA account from your pre-tax funds. Name it clearly at your brokerage (something like "Traditional IRA, Non-Deductible"). This makes tracking pre-tax vs. post-tax money dramatically simpler. Once you commingle the funds, every distribution and conversion requires pro-rata calculations across the entire balance. You will still need to file Form 8606, but separate accounts make the recordkeeping much cleaner. Your future self (and your tax preparer) will thank you.

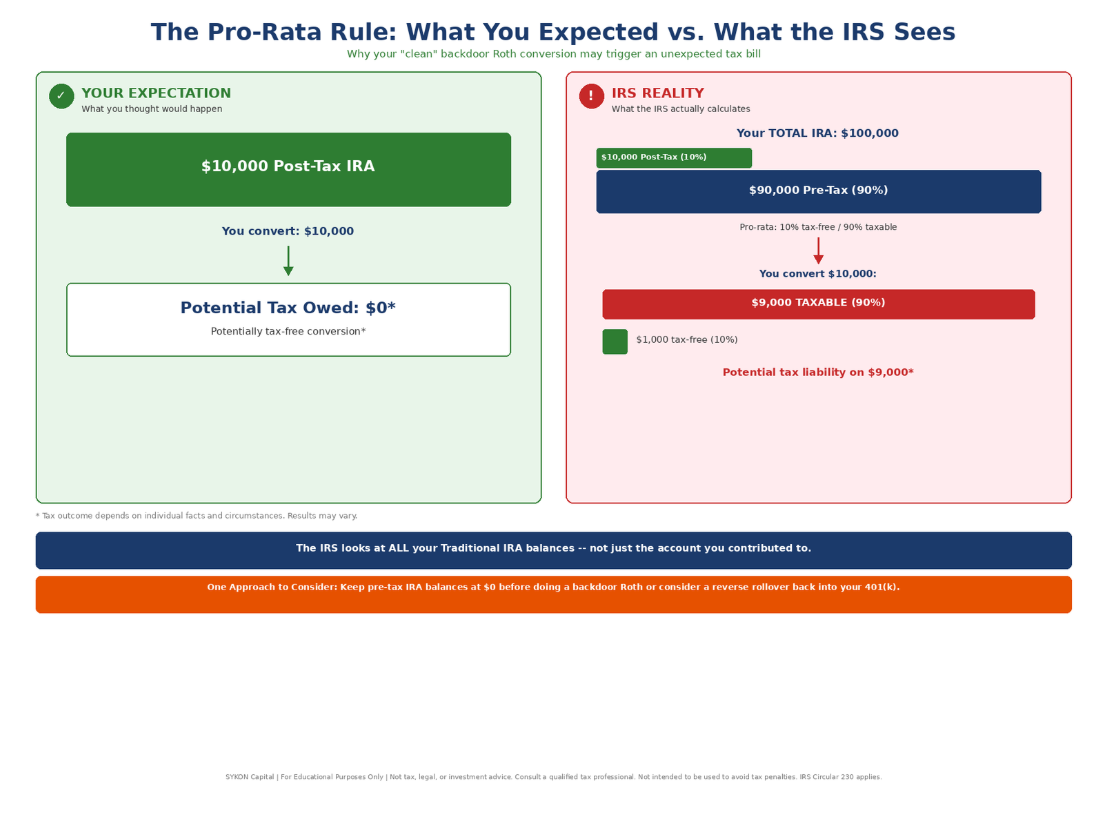

The Backdoor Roth Trap: The Pro-Rata Rule

The backdoor Roth IRA is one of the most popular strategies for high earners locked out of direct Roth contributions: make a non-deductible contribution to a Traditional IRA, then convert it to a Roth. Technically legal, widely used. But there is a trap that catches people every year: the pro-rata rule.

When you convert Traditional IRA money to a Roth, the IRS does not let you cherry-pick which dollars get converted. It looks at ALL of your Traditional IRA balances and calculates what percentage is pre-tax vs. post-tax. That ratio determines how much of your conversion is taxable.

Figure 3: The Pro-Rata Rule -- What You Expected vs. What the IRS Sees

You thought you were converting $10,000 potentially tax-free. Instead, the IRS treats 90% as taxable because 90% of your total IRA balance was pre-tax. The result: an unexpected tax bill on $9,000.

The 401(k) Rollover Warning

Rolling old 401(k) money into a Traditional IRA can sabotage your backdoor Roth strategy by dramatically increasing your pre-tax IRA balance. When you are young and considering a rollover, think carefully. Leaving old 401(k) money inside the plan (or rolling it into your current employer's plan) can preserve your backdoor Roth optionality for years.

If you already have pre-tax IRA money, some people use a "reverse rollover," moving that money back into their current employer's 401(k) to clear the pre-tax balance. This was exactly what the person in the Reddit post was attempting. Once the Traditional IRA is clean, you can execute a backdoor Roth potentially avoiding pro-rata complications.

WARNING: If you have ANY pre-tax IRA money (across all Traditional, SEP, or SIMPLE IRA accounts), the pro-rata rule applies. You cannot convert just your post-tax dollars cleanly.

Backdoor Roth IRA: Step-by-Step

Figure 4: How the Backdoor Roth IRA Strategy Generally Works (Educational Overview)

The Bottom Line: Proactive Beats Reactive

The person in that Reddit post is dealing with a tangle of recharacterizations, reverse rollovers, and Form 8606 filings that could have been avoided with upfront planning. These rules are genuinely complex, and the IRS does not make it easy.Whether you work with an outside accountant or handle things yourself, having an advisor who proactively thinks about these rules before you make changes can save enormous headaches. It is the difference between a clean, documented strategy and a panicked forum post in April. At SYKON Capital, this kind of proactive, year-round tax awareness is built into how we work with clients. Great advice is not just about what to invest in. It is about making sure the tax implications of every move are considered in advance, not discovered at tax time. Having enrolled agents who understand these rules at a granular level is a key part of how we deliver that.

If you are not sure where you stand on any of this, reach out before you make a contribution, not after.

About the Author

Todd Stankiewicz is Chief Investment Officer of SYKON Capital, a registered investment advisory firm with offices in Westchester County, NY and Jupiter, FL. As CIO, Todd leads portfolio construction, risk management, and investment strategy for the firm's client base, with direct experience helping investors navigate gated alternative structures including BREIT and Starwood. His work focuses on helping to identify structural risks in investment products before they become client problems, including liquidity mechanics, redemption dynamics, and valuation integrity in private markets. Todd also serves as Portfolio Manager of the Free Markets ETF (FMKT), a publicly traded fund focused on deregulation-driven investment themes.

SYKON Capital is a fee-based RIA registered with the U.S. Securities and Exchange Commission.

May 19, 2026

FAQ

Can I still contribute to an IRA after December 31? Yes, you have until April 15 of the following year. If your income is near the limit, file your taxes first, then contribute.

What happens if I contributed too much? Withdraw the excess before the deadline, recharacterize it, or pay a 6% penalty every year until it's fixed. Don't ignore it.

What is the pro-rata rule? The IRS looks at all your Traditional IRA balances when you convert to a Roth, not just the account you contributed to. Pre-tax money in any IRA makes part of your conversion taxable.

Can a 401(k) rollover hurt my backdoor Roth? Yes. Rolling old 401(k) money into a Traditional IRA increases your pre-tax balance and triggers the pro-rata rule. Consider keeping it in your employer's plan instead.

Disclaimer: This content is for educational purposes only and does not constitute tax, legal, or financial advice. The information presented is based on general tax rules as of the 2026 tax year and may not reflect your individual circumstances. Please consult a qualified tax professional or enrolled agent regarding your specific situation before taking any action. All figures cited are for the 2026 tax year and are subject to change.

IRS Circular 230 Disclosure: The tax information contained in this article is not intended to be used, and cannot be used, by any taxpayer for the purpose of avoiding tax penalties that may be imposed under the Internal Revenue Code. This content is provided for educational purposes only and does not constitute tax advice. Please consult a qualified tax professional or enrolled agent regarding your specific situation.

Sources

IRS Notice 2025-67: 2026 Retirement Plan Limits

CNBC: "IRS announces Roth IRA income limits for 2026"

Fidelity: "Roth IRA income limits for 2025 and 2026"

Vanguard: "Roth IRA income and contribution limits for 2026"